ANN ARBOR, MI / ACCESSWIRE / July 30, 2021 / University Bancorp, Inc. (OTCQB:UNIB) announced that it had an unaudited net income attributable to University Bancorp, Inc. common stock shareholders in 1Q2020 of $7,703,863, $1.62 per share on average shares outstanding of 4,765,518 for the first quarter, versus an unaudited net loss of $453,266, $0.09 per share on average shares outstanding of 5,204,899 for 1Q2020. For the 12 months ended March 31, 2021, net income was $35,859,946, $7.13 per share on average shares outstanding of 5,031,303 for the period.

Shareholders' equity attributable to University Bancorp, Inc. common stock shareholders was $58,579,620 or $12.19 per share, based on shares outstanding at March 31, 2020 of 4,765,518.

President Stephen Lange Ranzini noted, "The 1Q2021 result for profitability was excellent, despite lower industry-wide margins on mortgage loan originations during the quarter. Net income in the first quarter of each year is usually seasonally slow due to the lower pace of mortgage originations. Our internal model indicates that at current volumes of mortgage originations and current margins, $2.5 million per month of pre-tax income is possible, before any provisioning for potential or actual loan losses, or other unusual items."

At Midwest Loan Services, the increase in internal originations and organic growth of our sub-servicing clients led the number of mortgages serviced to grow 6.2% during 1Q2021, or annualized growth of 24.8%. Excluding the benefit from its $608.8 million of non-interest-bearing escrow deposits, Midwest Loan Services contributed $2.1 million in pre-tax income in 1Q2021, or an annualized pre-tax income run rate of $8.4 million.

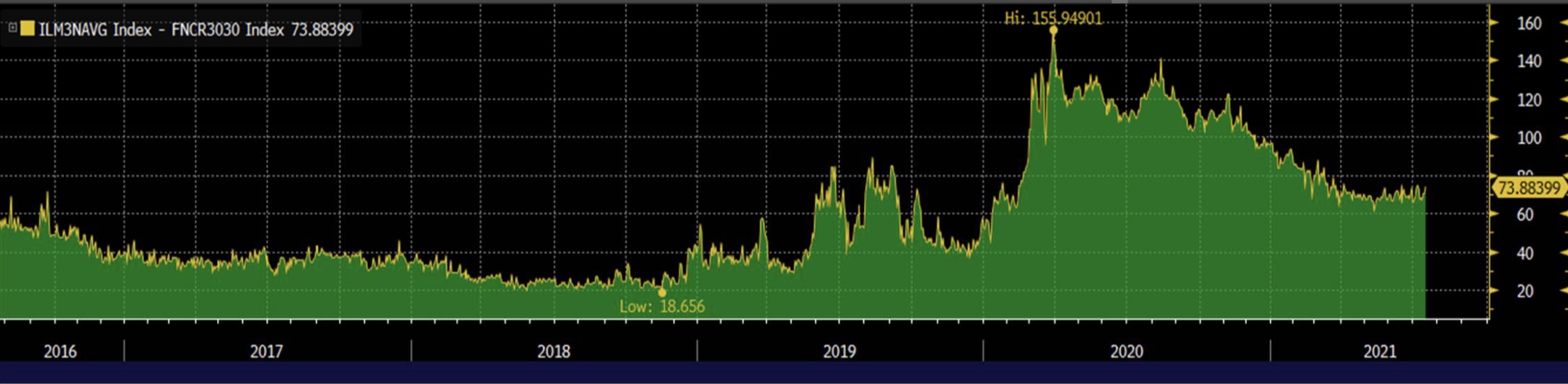

Results in 1Q2021 were positively impacted by above average margins on mortgage originations sold to the secondary market, which was caused by the pandemic and the Federal Reserve's reaction to it. The following graph is the best index that we are aware of for the overall industry-wide margins on standard FNMA and FHLMC loans sold in the secondary market.

Margins began to rise in mid-February 2020 and rose to record levels, as the industry struggled with capacity constraints caused by the surge in applications caused by record low interest rates, and financial and operational dislocations caused by the global pandemic. Margins have since moderated to lower but still elevated, mid-cycle levels.

Results in 1Q2021 were assisted by an unusual gain, which was partially offset by an unusual expense, which had an overall positive cumulative impact of $1,236,854, before tax:

Unusual gains:

- With the rise in long term mortgage interest rates during the quarter the valuation of our MSRs increased $1,571,041;

Unusual expenses:

- The fair market value of the hedged mortgage origination pipeline (FMV) fell $334,187 as the amount of locked loans fell over the level at year-end due to the rise in long term interest rates during the quarter.

Results in 1Q2020 were assisted by a seasonal factor, which were more than offset by three unusual expenses, which had an overall negative cumulative impact of $2,677,455, before tax:

Unusual gains:

- The fair market value of the hedged mortgage origination pipeline (FMV) rose $2,731,507 as the amount of locked loans rose over the seasonally low level at year-end and the pipeline of locked loans rose significantly due to record low mortgage interest rates;

Unusual expenses:

- With the fall in long term mortgage interest rates during the quarter the valuation of our MSRs decreased $4,007,633;

- Start-up expenses related to the American Mortgage Solutions division (AMS) were $1,080,329. As previously announced, a decision was made in early March 2020 to wind-down AMS's wholesale mortgage loan origination business;

- The Allowance for Loan Losses for general economic conditions and not tied to specific loans was increased by $321,000.

Mortgage origination volumes increased in 1Q2021, with closings of $546.0 million versus $403.9 million in 1Q2010, an increase of 35.2%. Each of our mortgage origination subsidiaries had strong volumes:

ULG: $299.5 million, up 74.7%, and purchase loans were up 53.3%;

UIF: $250.0 million, up 99.5%, and purchase loans were up 57.3%;

For 1Q2021, the Company had an annualized return on equity attributable to common stock shareholders of 59.7% on initial common stockholders' equity of $51,594,523. Return on equity over the trailing twelve months was 127.6% on initial equity attributable to common stock shareholders of $28,096,361.

Total Assets at 3/31/2021 were $653,014,241 versus $557,676,836 at 12/31/2020, $612,755,757 at 9/30/2020, $538,958,851 at 6/30/2020, $390,463,093 at 3/31/2020 and $361,956,924 at 12/31/2019.

The Tier 1 Leverage Capital Ratio at 3/31/2021 rose to 12.34% on net average assets of $464,126,000, from 11.27% at 12/31/2020 on net average assets of $464.1 million, 11.17% at 9/30/2020 on net average assets of $424.5 million, 10.44% at 6/30/2020 on net average assets of $387.3 million, 10.59% at 3/31/2020 on net average assets of $283.8 million and 8.15% at 12/31/2019 on net average assets of $299.1 million.

Basel 3 Common Equity Tier 1 Capital at 3/31/2021 was $52,069,000, at 12/31/2020 was $47,759,000, at 9/30/2020 was $43,108,000, at 6/30/2020 was $36,756,000, at 3/31/2020 was $27,308,000, and at 12/31/2019 was $23,179,000.

Cash & equity investment securities at the Company, available to meet working capital needs and to support investment opportunities at University Bank were $8,591,399. At 3/31/2021 the Company had no debt and one class of preferred stock outstanding convertible at $10 per share with a liquidation preference of $5,000,000.

Treasury shares as of 3/31/2021 were 441,381. During 3Q2021, the Company paid a total of $3,900,00, or the equivalent of $15.00 per share to acquire convertible preferred stock convertible into 260,000 shares of the Company's common stock, or 4.8% of the fully diluted shares of common stock at 3/31/2021.

Michigan and the Ann Arbor Metropolitan Statistical Area saw modest growth in employment in 1Q2021 amid continuing high levels of unemployment. Despite this, the performance of our portfolio loans and our overall asset quality continues to perform well, with lower loan delinquencies, however we are experiencing a rise in loans classified as substandard. We had no foreclosed other real estate owned property at quarter-end, and substandard assets rose 125% during 1Q2021 to $1,407,199, 2.69% of Tier 1 Capital at 3/31/2021. The allowance for loan losses stood at $4,000,000 or 2.69% of the amount of portfolio loans, excluding the loans held for sale.

At 3/31/2021, we had the following with respect to delinquent loans (including both delinquent portfolio loans and delinquent loans held for sale):

Delinquent 30 Days to 59 Days, $778,000

Delinquent 60 Days to 89 Days, $211,000

Delinquent Over 90 Days & on Non-Accrual, $386,000+

+This balance consisted of two well secured residential loans. In addition, we owned the MSRs on $15,875,834 in GNMA pool related residential mortgage loans that have reached 90 days delinquency status and are therefore included on our balance sheet per GAAP. These loans are guaranteed as to principal 100% by FHA.

Other key statistics as of 3/31/2021:

| · 10-year annual average revenue growth*, | 25.80% |

| · 5-year annual average revenue growth*, | 29.70% |

| · 1Q2021 vs. 1Q2020 revenue growth*, | 95.80% |

| · TTM Revenue | $154,130,247 |

| · 10 Year Average ROE | 22.90% |

| · 5 Year Average ROE | 36.40% |

| · LLR/NPAs>90 % | 669.70% |

| · Debt to equity ratio, | 0% |

| · Current Ratio,# | 97.1x |

| · Efficiency Ratio, %+ | 69.10% |

| · Total Assets, | $557,676,836 |

| · Loans Held for Sale, before Reserves, | $165,136,427 |

| · NPAs >90 days | $597,305 |

| · TTM ROA % | 8.41% |

| · TCE/TA % | 10.04% |

| · Total Capital Ratio % | 13.53% |

| · NPAs/Assets % | 0.25% |

| · Texas Ratio % | 2.35% |

| · NIM % | 2.48% |

| · NCOs/Loans % | -0.01% |

| · Trailing 12 Months P-E Ratiox | 2.1x |

*Using 1Q2021, 1Q2020, 2020, 2019, 2018, 2017, 2016, 2015 and 2010 revenue which were $35,022,290, $17,883,554, $136,991,511, $69,112,502, $55,988,570, $54,493,179, $50,948,149, $43,644,425 and $20,437,724, respectively.

# Parent company only current assets divided by 12-month projected cash expenses.

+ Calculated as: (non-interest expense/(net interest income + non-interest income))

x Based on last sale of $15.07 per share.

Excluding goodwill & other intangibles related to the acquisition of Midwest Loan Services and Ann Arbor Insurance Center, net tangible shareholders' equity attributable to University Bancorp, Inc. common stock shareholders was $57,587,672 or $12.08 per share at 3/31/2021. Please note that we view the current market values of our insurance agency and Midwest Loan Services as substantially in excess of their carrying value including this goodwill.

Shareholders and investors are encouraged to refer to the financial information including the investor presentations, audited financial statements, strategic plan and prior press releases, available on our investor relations web page at: http://www.university-bank.com/bancorp/ .

Ann Arbor-based University Bancorp owns 100% of University Bank which, together with its Michigan-based subsidiaries, holds and manages a total of over $36 billion in financial assets for over 191,000 customers, and our over 560 employees make us the 5th largest bank based in Michigan. University Bank is an FDIC-insured, locally owned and managed community bank, and meets the financial needs of its community through its creative and innovative services. Founded in 1890, University Bank® is the 15th oldest bank headquartered in Michigan. We are proud to have been selected as the 'Community Bankers of the Year' by American Banker magazine and as the recipient of the American Bankers Association's Community Bank Award. University Bank is a Member FDIC. The members of University Bank's corporate family, ranked by their size of revenues are:

- University Lending Group, a retail residential mortgage originator based in Clinton Township, MI;

- Midwest Loan Services, a residential mortgage subservicer based in Houghton, MI;

- UIF, a faith-based banking firm based in Southfield, MI;

- Community Banking, based in Ann Arbor, MI, which provides traditional community banking services in the Ann Arbor area;

- Midwest Loan Solutions, a reverse residential mortgage lender and warehouse lender based in Southfield, MI;

- Ann Arbor Insurance Centre, an independent insurance agency based in Ann Arbor.

CAUTIONARY STATEMENT: This press release contains certain forward-looking statements that involve risks and uncertainties. Forward-looking statements include, but are not limited to, statements concerning future growth in assets, pre-tax income and net income, budgeted income levels, the sustainability of past results, mortgage origination levels and margins, valuations, and other expectations and/or goals. Such statements are subject to certain risks and uncertainties which could cause actual results to differ materially from those expressed or implied by such forward-looking statements, including, but not limited to, economic, competitive, governmental and technological factors affecting our operations, markets, products, services, interest rates and fees for services. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release. We undertake no obligation to update any information or forward-looking statement.

Contact:

Stephen Lange Ranzini, President and CEO

Phone: 734-741-5858, Ext. 9226

Email: ranzini@university-bank.com

SOURCE: University Bancorp, Inc.

View source version on accesswire.com:

https://www.accesswire.com/657787/University-Bancorp-1Q2021-Net-Income-7703863-162-Per-Share