2025 First Quarter Financial Highlights:

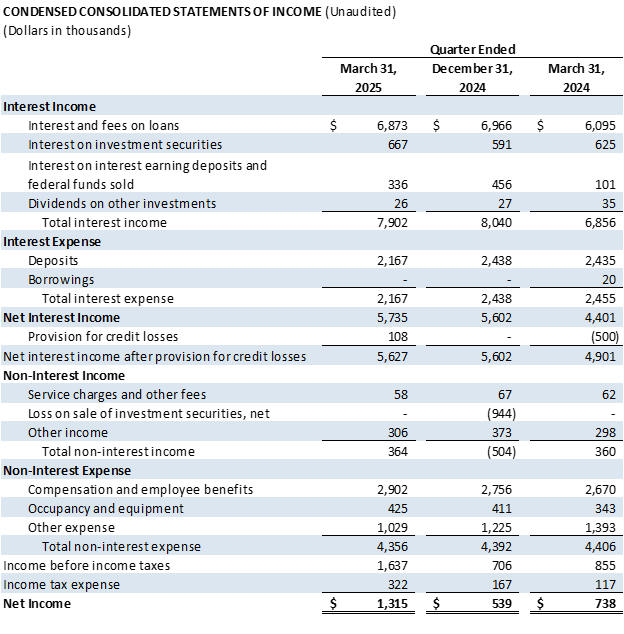

Net income was $1.3 million compared to $539,000 for the fourth quarter of 2024.

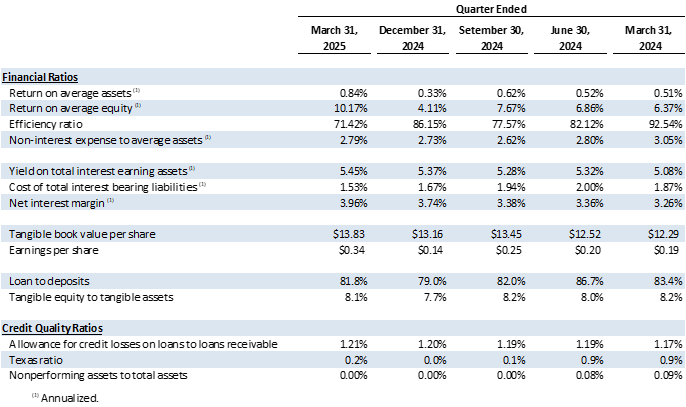

Loans receivable increased $6.7 million, or 5.83% annualized growth rate.

Net interest margin increased 22 basis points ("bps") to 3.96% from 3.74% for the fourth quarter of 2024.

Total cost of deposits decreased 14 bps to 1.53% from 1.67% for the fourth quarter of 2024.

The Bank had no nonperforming assets during the first quarter of 2025.

Headquarters was moved to 1313 Broadway, Suite 400 Tacoma, WA (Commencement Bank Plaza).

Capital ratios remained well above regulatory requirements.

TACOMA, WA / ACCESS Newswire / April 23, 2025 / Commencement Bancorp, Inc. (OTCQX:CBWA) (the "Company", "we," or "us"), the parent company of Commencement Bank (the "Bank") reported net income of $1.3 million, or $0.34 per share, for the first quarter of 2025, compared to $539,000, or $0.14 per share, for the fourth quarter of 2024 and $738,000, or $0.19 per share, for the first quarter of 2024.

During the fourth quarter of 2024, the Bank executed two strategic measures impacting financial results. First, the Bank incurred an after-tax loss of $745,000 on the sale of certain investment securities due to the strategic repositioning of its balance sheet. Second, the Bank sold certain company-owned life insurance policies resulting in recognition of tax expense of $104,000. The after-tax impact of these transactions for the fourth quarter of 2024 was $0.22 per share.

"The Bank's financial performance in first quarter centers around our increased operating efficiencies and reduction in cost of funds. This quarter also saw the long-awaited move to the Bank's new headquarters at 1313 Broadway in downtown Tacoma, proudly named the Commencement Bank Plaza. The new space allows the entire team to be on one floor, which has increased collaboration and efficiency, resulting in better production and engagement. We look forward to sharing our new location with shareholders, clients, and community members at our grand opening in mid-June," said John E. Manolides, Chief Executive Officer.

"We have continued to retain our deposit relationships over the course of first quarter and have done an incredible job in growing new relationships. Our team is proactive and nimble, allowing us to compete on every level regardless of the challenges. We're in a good position for continued growth," said Nigel L. English, President & Chief Operating Officer.

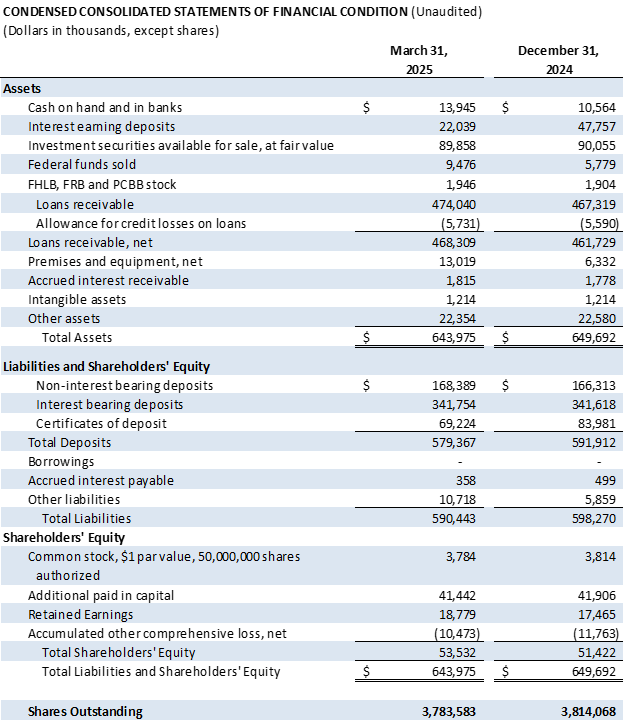

Balance Sheet

Interest earning deposits decreased $25.7 million to $22.0 million at March 31, 2025 compared to $47.8 million at December 31, 2024 primarily due to a decrease in customer deposits.

Investment securities available for sale decreased $197,000, or 0.2%, to $90.0 million at March 31, 2025 from $90.2 million at December 31, 2024 due to principal payments and amortization of $2.2 million, offset by a decrease in unrealized losses of $2.0 million. The decrease in market rates at March 31, 2025 caused the decrease in unrealized losses.

Loans receivable increased $6.7 million, or 1.4%, to $474.0 million at March 31, 2025 from $467.3 million at December 31, 2024 due primarily to new loan originations, offset by principal payments. The Bank originated commitments of $20.8 million during first quarter of 2025 compared to $13.4 million during the fourth quarter of 2024 and $33.6 million during the first quarter of 2024.

Total deposits decreased $12.5 million, or 2.1%, to $579.4 million at March 31, 2025 from $591.9 million at December 31, 2024. Noninterest bearing deposits, as a percentage of total deposits, was 29.1% at March 31, 2025.

Credit Quality

The Bank had no nonperforming assets at March 31, 2025 or December 31, 2024. The allowance for credit losses to loans receivable remains strong at 1.21% at March 31, 2025.

The percentage of classified loans to loans receivable was 2.13% at March 31, 2025 compared to 1.82% at December 31, 2024 due primarily to the downgrade of two credit relationships from Watch status. Classified loans include loans rated Substandard or worse. The 2024 financial results of certain classified loans indicate credit improvements, and the Bank anticipates upgrades during the third quarter of 2025 if sustained performance can be maintained. The Bank proactively downgrades loans if the borrower is experiencing financial difficulties.

Liquidity

The Bank has ample liquidity with both on- and off-balance sheet sources. Total on-balance sheet liquidity of $121.0 million, or 18.8% of total assets at March 31, 2025, includes cash and cash equivalents and unencumbered investment securities. The Bank has access to Federal Home Loan Bank advances, Federal Reserve discount window, and Federal Funds lines with correspondent banks of $227.7 million at March 31, 2025. The Bank can also access brokered deposits with policy limits of 25% of total deposits, totaling $144.9 million at March 31, 2025.

Income Statement

Net interest income increased $133,000, or 2.4%, during the first quarter of 2025 compared to the fourth quarter of 2024 due to the decrease in interest expense of $271,000, offset by the decrease in interest income of $138,000. Net interest margin increased 22 bps to 3.96% during the first quarter of 2025 from 3.74% during the fourth quarter of 2024.

Interest on interest earning deposits and Federal Funds Sold decreased $120,000 during the first quarter of 2025 compared to the fourth quarter of 2024 due to a decrease in the average balance of $6.4 million. Additionally, the yield decreased due to the 50 bps reduction in the short-term market rates during the fourth quarter of 2024.

Interest income on loans decreased $93,000 during the first quarter of 2025 compared to the fourth quarter of 2024 due to the number of days in the quarter and the impacts of the 50 bps rate cuts during the fourth quarter of 2024, primarily on variable rate loans. The quarterly average balance of variable loans tied to Prime was $84.7 million during the first quarter of 2025. The Bank experienced an increase in the average balance of loans of $1.7 million. The yield on loans increased one bp to 5.99% for the first quarter of 2025 from 5.98% for the fourth quarter of 2024 due to loan mix, higher yields on new originations, and repricing higher on existing portfolio rates. Additionally, during the fourth quarter of 2024, a prepayment penalty and deferred fees recognized on significant loan payoffs accounted for four bps of yield.

Interest income on investment securities increased $76,000 during the first quarter of 2025 compared to the fourth quarter of 2024 due to the repositioning of the portfolio in December 2024. The yield on securities increased 49 bps to 3.03% during the first quarter of 2025 compared to 2.54% during the fourth quarter of 2024.

Interest expense on deposits decreased $271,000 during the first quarter of 2025 compared to the fourth quarter of 2024 due to a decrease in costs of 22 bps and, to a lesser extent, a decrease in the average balance of $407,000. Total cost of deposits decreased 14 bps to 1.53% for the first quarter of 2025 compared to 1.67% for the fourth quarter of 2024 due to the reduction of rates for exception-priced deposits commensurate with the decreases in the market rates.

Total non-interest income increased $868,000 during the first quarter of 2025 compared to the fourth quarter of 2024 due to the loss on sale of investments of $944,000 recognized in 2024. Excluding the loss on sale, non-interest income decreased $76,000, or 17.3%, due to recognition of loan swap fee income of $22,000 and higher customer-related transactional activity in 2024.

Total non-interest expense decreased $36,000, or 0.8%, during the first quarter of 2025 compared to the fourth quarter of 2024 due primarily to one-time charges recorded in 2024. Compensation and employee benefits increased during the first quarter of 2025 due to increases in salaries and related benefits. The first quarter of 2025 also includes one month of lease amortization and depreciation of assets related to the new Tacoma headquarters as well as all moving costs.

###

About Commencement Bancorp, Inc.

Commencement Bancorp, Inc. is the holding company for Commencement Bank, headquartered in Tacoma, Washington. Commencement Bank was formed in 2006 to provide traditional, reliable, and sustainable banking in Pierce, King, and Thurston counties and the surrounding areas. Their team of experienced banking experts focuses on personal attention, flexible service, and building strong relationships with customers through state-of-the-art technology as well as traditional delivery systems. As a local bank, Commencement Bank is deeply committed to the community. For more information, please visit www.commencementbank.com. For information related to the trading of CBWA, please visit www.otcmarkets.com.

For further discussion, please contact the following:

John E. Manolides, Chief Executive Officer | 253-284-1802

Nigel L. English, President & Chief Operating Officer | 253-284-1801

Brandi Parker, Executive Vice President & Chief Financial Officer | 253-284-1803

Forward-Looking Statement Safe Harbor: This news release contains comments or information that constitutes forward-looking statements (within the meaning of the Private Securities Litigation Reform Act of 1995) that are based on current expectations that involve a number of risks and uncertainties. Forward-looking statements describe Commencement Bancorp, Inc.'s projections, estimates, plans and expectations of future results and can be identified by words such as "believe," "intend," "estimate," "likely," "anticipate," "expect," "looking forward," and other similar expressions. They are not guarantees of future performance. Actual results may differ materially from the results expressed in these forward-looking statements, which because of their forward-looking nature, are difficult to predict. Investors should not place undue reliance on any forward-looking statement, and should consider factors that might cause differences including but not limited to the degree of competition by traditional and nontraditional competitors, declines in real estate markets, an increase in unemployment or sustained high levels of unemployment; changes in interest rates; greater than expected costs to integrate acquisitions, adverse changes in local, national and international economies; changes in the Federal Reserve's actions that affect monetary and fiscal policies; changes in legislative or regulatory actions or reform, including without limitation, the Dodd-Frank Wall Street Reform and Consumer Protection Act; demand for products and services; changes to the quality of the loan portfolio and our ability to succeed in our problem-asset resolution efforts; the impact of technological advances; changes in tax laws; and other risk factors. Commencement Bancorp, Inc. undertakes no obligation to publicly update or clarify any forward-looking statement to reflect the impact of events or circumstances that may arise after the date of this release.

SOURCE: Commencement Bancorp, Inc.